At a glance

- A blockchain system enables transactions to be written directly into a single register, which creates an interlocking system of records.

- Experts agree that blockchain will not disrupt the industry any time soon, but its efficiencies should not be underestimated or ignored.

- With the increasing adoption of blockchain technology, the role of an accountant will change but not be eliminated.

In a perfect world, blockchain and the world of accounting would be close bedfellows, working side by side to create the perfect system of asset recording, storage and administration.

Blockchain records and stores assets, liabilities and transactions, and provides methods of recording cash flow and reconciling accounts. It doesn’t offer double-entry bookkeeping, but multiple entry, with its new distributive ledger technology. It sounds tailor-made for the world of accounting, a system ready to wear and fit for purpose.

Here’s a system that doesn’t need separate records based on transaction receipts, a system where transactions are written directly into a single register, which then creates an interlocking system of records – or “blocks” of information – that is automatically verified, and can be viewed by, all users.

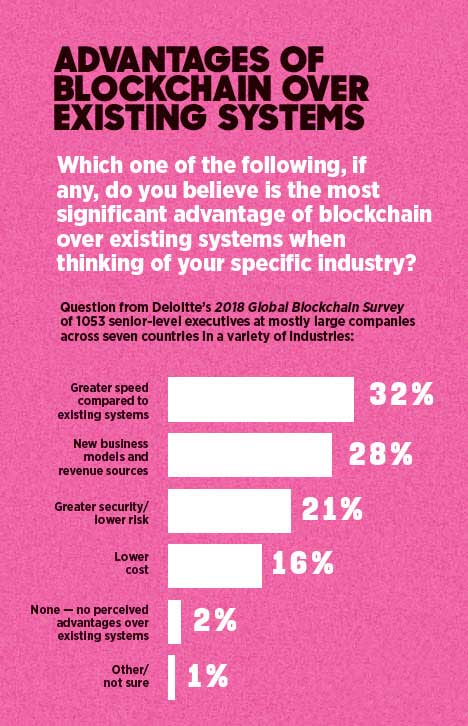

Blockchain proponents say accountancy remains a legacy-driven business, relying on paper trails and even legacy software to perform many of its functions. It needs paper trails to ensure that regulatory requirements are met, and it still requires the independent auditor, charged with forensic skills, to check back on a company’s financial information.

Each audit is an exercise in supervision. The proving and verification of a set of accounts keeps a small army busy for long periods of time.

All in favour of blockchain...

Blockchain appears to be screaming to accountants, and many other professionals, that the third parties they have relied on for years are becoming redundant.

A decentralised system is coming. All entries will be distributed and cryptographically sealed, so the chances of destroying or manipulating them to conceal activity are practically impossible.

Audits will be far more automated without the need to pore through paper trail documents. Auditors will be able to speedily verify key data underpinning financial statements, thus reducing cost and time. Regulatory compliance can be verified far more efficiently.

Bring on this brave new world, they are saying. Why are you waiting?

The blockchain critics say...

In a not-so-perfect world, there are other considerations. Fear is one of the reasons, fear of how technology will disrupt an industry that has depended for so long on human oversight and scrutiny. Jobs will be affected, too, even if that’s rarely an issue for most corporations.

Cost, not staff numbers, is what keeps the C-suite awake at night, and blockchain in its present form remains very costly. There are also questions about a blockchain system’s data storage capacity and speed, as well as its applicability.

Some say blockchain is a system looking for a solution. There are other relational databases that can do much the same, which exist now and can be implemented more cheaply. These allow records to be encrypted, rendering them unalterable and permitting them to be distributed across multiple locations. Auditors will be able to speedily verify key data underpinning financial statements, thus reducing cost and time.

Blockchain is a proven instantaneous record keeper and storage system for information, but beyond that, it remains mostly in the realm of proof-of-concept, an excellent aide for inventory and supply chain management.

The best-known examples are Walmart, which has put all its fresh food suppliers on a blockchain-enabled system, and shipping line Maersk, which has developed a system called TradeLens, which uses a blockchain system to digitalise its entire supply chain. Cross-border payments are said to be next in line for multiple ledger adaptation.

Blockchain's early adopters

Most early participants remain cautious but optimistic. Among them is Craig Fischer, innovation program manager at the Bureau of the Fiscal Service at the US Treasury. Fischer is leading the charge among US federal divisions to advance the government’s understanding of blockchain. His intention was always to start agnostic, ignore the hype and take the system at face value.

The bureau has just completed a successful proof-of-concept using blockchain to track, manage and transfer mobile devices and, in a second case, aims to do much the same for software packages, ensuring that there are no unused, missing or out-of-date software licences.

“Every year we would go through this labour-intensive process – to track all the US Treasury phones,” Fischer explains.

“It has meant sending five or six people out to locate the phones of about 3500 people around six different geographical locations across the US.” The trial amounted to similar “pain points” as Fischer describes them. All the phones had to be hunted down, but with blockchain they would be scanned, logged and registered to a distributive ledger system.

It was hard work, but by the trial’s end, the new system offered startling efficiencies.

“I can now tell if Craig Fischer is using his phone and where he is at any point of time,” Fischer says.

With this knowledge he can set up smart contracts in the system. “If Craig hasn’t logged onto his phone in two weeks, then we send him an email,” he says. The blockchain doesn’t lie.

“Doing this has gone from a passive, annual inventory to a very active knowledge of current activity,” he says.

How far would he take the system? Fischer says the next step is likely to be tracking software licences, which cost the US federal government about US$8 billion a year.

“A person using a licence may leave for another job and sometimes we don’t recycle that licence to a new user. We haven’t been managing it well,” he admits.

“The question is can we go forward and manage it in real time – see who’s using it and, if not, repurpose it for another user who would use it, rather than continually rebuying new software? We have looked at this from an enterprise-wide perspective – for the entire federal government – and it makes a lot of sense.”

A new system of exchange would then come into being and from that, Fischer explains, a new set of standards would be created for the buying, exchanging and/or repurposing of software licences.

Does Fischer believe blockchain can be repurposed, so to speak, for accounting? He uses an analogy of mechanics. Not so long ago we would take a car to the mechanic and they would figure out what was physically wrong. Now the same mechanic uses computer diagnostics. “You still need the mechanic, but the mechanic will have new things to learn,” he says.

“With financial management and accounting, the people who occupy these roles will still be needed, but if you look at their roles within robotics and blockchain, they will have new skills to learn.”

Blockchain optimism

Arguably more bullish about the future of blockchain is Nathana O’Brien Sharma, program director, blockchain, policy, law and ethics at Singularity University in Silicon Valley. Sharma also has skin in the game as general counsel at Labelbox, one of the better-known artificial intelligence start-ups in Silicon Valley.

Like Fischer, Sharma agrees that blockchain is not disrupting the industry any time soon, but its efficiencies can’t be underestimated or ignored. Humans will not be out of the equation for quite some time, Sharma says, but in the meantime, accountants are doing themselves a huge disfavour by not testing these new tools.

“Right now, accountants have an impossible job – they are there to detect fraud, to find problems and anomalies, but there’s just so much information and data out there, it’s impossible for any one person or group of people to review it,” Sharma says.

“The new technology will be even more secure to work on, and it means the costs will go down and accountants can spend their time on the highest leveraged activities.”

Sharma says this is about evolution. Consider the accountant’s role before Excel spreadsheets, she says. “They all thought Excel would do our work for us, but it didn’t. But it is a better spreadsheet and made the job easier.

"If you don't experiment with [blockchain], you will be in danger of falling behind."

“Think about being an accountant without Excel or QuickBooks or without the many tools they need to make themselves highly effective, and now think of blockchain as yet another tool.”

Sharma is not saying entire accounting systems should be converted to customer facing blockchains tomorrow. She is also aware of the criticism levelled at blockchain, not the least by McKinsey in its now highly reported statement that blockchain is in its infancy and is “relatively unstable, expensive and complex”.

The McKinsey report asks why we have to resort to blockchain when there are traditional relational databases that can be tweaked to allow records to be encrypted, rendered unalterable and distributed across multiple locations.

Sharma’s answer is that technology is changing at an exponential rate and that ignorance or apathy will put the slower movers at a disadvantage. “You don’t have to focus all your time and energy on it. That said, if you don’t run a pilot, it’s going to be hard to be a fast follower,” she says.

Sharma believes that the first movers in artificial intelligence will receive the higher returns on initial investment and the remaining “fast followers” will get the crumbs.

“McKinsey is right. It is expensive and it is complex, but if you don’t experiment with it, you will be in danger of falling behind.”

The adoption by some high-profile names is proof that blockchain is on the rise, says Sharma. Some of the largest financial institutions in the US are using it – IBM has been testing a Blockchain World Wire payment network, Nasdaq and Citibank use it to automate payment processing from Citibank to Nasdaq’s blockchain, JPMorgan has submitted a patent for applying distributed ledger technology for settling transactions between banks, and Fidelity is using it for custodial services.

Sharma also believes that blockchain could well have raised red flags to some of the more egregious aspects of the global financial crisis. It would have helped foster an understanding of the sub-prime products and their inherent instability.

CPA Library member resource:

“We see all these sub-prime loans being packaged and sliced up and then there were derivatives on these loans. We got a house of cards of derivatives that was built on nobody understanding what was going on, what was connected to what or what was being bought.”

If financial products could have been tracked more efficiently, she argues, the problem may have never occurred.

“We could have seen and understood which mortgages were being packed up to create a derivative. Instead of being opaque, we could have stepped back, looked at the distributive ledger and everybody would have seen the information.”

In the end, should accountants be worried about the arrival of blockchain? Sharma thinks not. Remember when you first saw the internet? What about when you first received a personal computer or a laptop? It’s the same, she says – it’s just another tool.

“It’s a new tool that will change the role, but not make it obsolete. Those accountants who can embrace new technology, artificial intelligence and blockchain will be well ahead of the game.”

Accounting and blockchain

It’s a common mantra in the financial services industry that professionals will still be needed when blockchain arrives in force, and they will just be using more powerful tools. All the same, Fischer does not believe the accounting world is that close to using blockchain throughout its processes. “We don’t know how realtime reconciliations will work – the technology has to evolve before we get there, and there is always the need to track a physical asset, which will require people to monitor and track them.”

The accountant’s role will change, but it will not be eliminated. Information must still be interpreted and categorised correctly before it is entered into a blockchain. It will be the accountant’s job to do this, as well as implement and maintain the system.

Bookkeepers, too, will not be redundant. Who else will oversee accounts receivable? Who else will oversee contracts for payments for goods and services? Who else will prepare invoices, and track income and costs?

Even with blockchain technology, people are needed to enter contracts, purchase orders and make payments into these multiplying blocks. It will provide efficiency, record permanency and transparency. Seen in this light, it’s likely to be something bookkeepers and accountants should be fighting for, rather than something they should fear.